Spotify: almost a goodbye after a +450% love story

Why I sold: thesis exhaustion and risks

In today’s deep dive:

My original Spotify thesis breakdown and its evolution over the past 5 years

The risks leading me to sell 90% of it, first bought in in 2021

What would bring me back in - with some questions I’d pose to the CEO today

5 years earlier…

In late 2021, Spotify was trading around $230/share.

I had been observing the stock for the whole year: back then I was still a part-time guitar player and somehow I had been attached to the company since 2014, when their revolutionary freemium business model brought music in my life with an unprecedented intensity!

For the whole first semester of 2021, the valuation looked too expensive from all angles. Then suddenly, a vicious crash down to the $200s.

So, I took the chance to drill down into the fundamental business trajectory and here’s what I saw:

1: A Pricing Power candidate with declared Gross Margin expansion on the way

At the time, Spotify’s Gross Margin sat around 25% - a number that scared off most value-oriented investors (I also normally set the bar beyond 50%: basically, I broke my own rules).

At the same time though, Management was pointing to a ramp-up towards 35%, thanks to a favorable segment mix shift: audiobooks and advertising revenue growing faster than Premium subscriptions, both carrying structurally higher margins than the core music licensing.

Here’s the math that excited me: if a mid-point Gross Margin of 30-32% could be achieved without a proportional increase in OPEX, that would have unlocked a recurring pattern of profitability, with a first real earnings surprise for institutional investors who were counting out the company.

2: Even modest profitability would’ve generate monster ROICs.

Given Spotify’s extremely asset-light capital structure, even an earnings power between 5% and 10% would have translated into 25%+ Returns on Invested Capital.

And that’s the flywheel I very often mention: ROIC → FCF generation → reinvestment into growth → network effects compounding.

The classic C2C (consumer-to-consumer) platform dynamic.

And we know it: Mr. Market loves high ROIC.

3: Valuation hit “makes-no-sense” absurdity in 2022

As I always mention, stock prices trade 95% of the time either overvalued or undervalued, and that’s why seeking a perfect “fair value” zone does not make any sense.

But 5% of the time, they reach absurdity in either ways: so insanely cheap, or so insanely expensive.

In 2022, it happened to SPOT too.

Now look, I know Price-to-Sales is a false friend that leads to many mistakes. But hear me out.

In 2022, Spotify’s market cap cratered to roughly $15B.

The company was building a network dominance on the way to 1 billion MAUs, with forward revenues of $16-18B.

That’s a sub-1x P/S for the dominant network platforms on Earth.

It didn’t make much sense. This is where I doubled-down heavily.

4: The Network Power was real + Expansion of multi-verticals

Almost 1 billion people on the platform despite multiple consecutive price hikes.

Pricing Power was visible.

But most importantly: the opportunity for multiple verticals was clearly keeping ARPU untapped.

Podcasts and audiobooks were on the way, but Management was also talking about future verticals like merch, DTC superfan experiences, ticketing…

Daniel Ek once said out loud: “We’ll be doing 100 billion in sales at some point.”

An exaggeration? Probably.

But the ambition behind the vision was exactly what I wanted from a Founder-CEO.

Mid-Way: The Emotional Rollercoaster

My first 2 years as shareholder were horrible (it happens quite frequently).

I started buying around $230/share. I then saw the stock cratering to $67.

That’s a -70% drawdown.

At some poing, I was down -55% as I was trying to calibrate a catious accumulation plan.

But overall, I just stayed the course.

Not because I’m immune to volatility, but because I wasn’t seeing any permanent thesis breaker. The fundamentals were tracking towards the plan: MAU growth accelerating, Gross Margin slowly improving, the podcast and audiobook bets taking shape.

But let me be fully transparent here.

The crash did trigger underconfidence, impatience, and defeat.

At -50%, I was questioning myself.

But nonetheless, I averaged down 13 or 14 times during that period.

Without any doubt, this company is one of those investments that made me a better investor.

Not because of the returns. Because of the emotional rollercoaster it forced me to experience.

Because the following season in price action was even more difficult.

I observed the recovery above my average purchase price. I watched the stock climb back to my initial entry point. And so many times I had the temptation to sell and just capture my gains.

Also because the position size was becoming very significant, above 15%.

I actually did sell a piece, at around $320. Long-time readers may remember: I rotated some capital into another opportunity. With the benefit of hindsight, that looked like a mistake on the Spotify side - but the other stock 3x-ed meanwhile, so the overall ROI from that rotation was actually even better.

I also had a valuation-driven sell button around $750-800, following my bull case scenario.

So I didn’t sell more on the way to $700, and just let the compounder run.

Coming to our trading days, this clearly means that I didn’t catch the top when I sold and that’s fine.

I sold the remaining 90% of SPOT at $550 on average, at around +450% in profit.

Let's see why more in detail.

The fundamental risks behind my sale

I could argue that the initial thesis has played out.

Gross Margin hit 32.5% on the way to the original goal. The segment mix is partially executing. Full-year 2025 delivered €2.9B in Free Cash Flow and profitability on a recurring positive pattern, awakening “sleeping” institutionals.

But now a 450%+ return, the risk-reward has fundamentally changed, while other opportunities seem to rise under my eyes.

The Spotify Thesis Exhaustion:

⚠️ R1: Where are the other verticals?

Daniel Ek’s grand vision of Spotify as a multi-vertical platform (merch, DTC experiences, superfan tiers, ticketing) has not been materializing. Yes, Spotify contributed to $1B in ticket sales in 2025. Yes, the superfan concept exists.

But scan the latest earnings call transcript. You won’t find “DTC” or “merch” as strategic pillars. The new leadership seems really AI-first.

I would like to thank musicben of STVDIO+ for providing such valuable insight on the latest conference call:

The multi-vertical playbook that underpinned my original thesis has been de-prioritized.

⚠️ R2: The new advertising model seems far from inflection

Spotify launched Ad Exchange (SAX)in April 2025: a programmatic, auction-based DSP platform integrated with The Trade Desk, Google DV360, Amazon DSP, Magnite, and others.

While this is potentially massive, Management just pointed out that the “inflection point” is still far away:

Ad-Supported revenue in Q4 2025 was down 4% year-on-year in reported terms (up just 4% in constant currency). Management themselves have acknowledged the ramp-up to meaningful inflection is still ahead. And this sort of uncertainty is not healthy.

For this to become a real driver of Gross Margin expansion, we need to see a massive ramp-up in ads bids which frankly I can’t see materializing in the next 12 months.

⚠️ R3: Will AI make music streaming a commodity?

Suno is an example of how quickly new entrants can emerge, go viral, and build a network in the AI-generated music space.

Is this an existential threat? Maybe not today. But it injects uncertainty into the durability of the Network MOAT.

We’re seeing a massive shortening of the time needed for viral platforms to reach millions of users. I honestly wouldn’t be surprised to see the “time-to-1M-users” come down to hours for a new streaming platform.

⚠️ R4: Daniel Ek, the “multi-vertical CEO” stepping down

As of January 1, 2026, Daniel Ek is no longer CEO. He moved to Executive Chairman.

The new co-CEOs are Alex Norström (Chief Business Officer) and Gustav Söderström (Chief Product & Technology Officer). Both 15+ year Spotify veterans. Both competent.

But Ek was the visionary behind the multi-vertical expansion. Söderström’s background is heavily tech and AI-focused. Norström runs commercial operations.

The message behind this transition? The company doubles down on product and AI at the expense of the bold platform bets.

It’s not a bad pivot. But it’s a different thesis than the one I bought into.

⚠️ R5: Gross Margin ceiling is real

In a business model like Spotify’s, Gross Margin expansion through “Business Model Transformation” is what I call the turbo-trigger (taken from the book Expectations Investing).

Think of Uber: if they can squeeze COGS through autonomous driving, the earnings surprise would be dramatic.

For Spotify though, GM seems structurally capped.

Some COGS will always be inevitable.

The music labels will never allow Spotify to create its own music labels. That would trigger an immediate domino of artists leaving the platform, eroding the very network effects and pricing power that make the business valuable.

I have a Checklist to investigate the levers for Gross Margin Expansion, but none seems to offer an underappreciated catalyst.

🚫 Pricing power

How much further can prices go? US Premium just went from $11.99 to $12.99. Apple Music and Amazon Music fall below that. Maybe there’s still room, but there must be a ceiling at some point.

🚫 Segment mix

Already partially executed. Audiobooks and podcasts help, but music is still about 88% of Premium revenue.

As mentioned, the ramp-up of new verticals is lagging.

🚫 Scale efficiencies

The company’s penetration is already remarkable.

About 75% of new subscribers are coming regions with structurally lower ARPU. North American subscriber growth was just +3.25% YoY in Q3 2025. Saturation in developed markets is approaching.

🚫 Vertical integration

Impossible with labels, as explained.

🚫 Business Model Transformation

This last point doesn’t need further explanations.

→ The bottom line: a path from 33% to 40%+ Gross Margin looks hard to visualize from here.

Valuation as confirmation point

Selling is easier when both qualitative and quantitative evidence come together.

Running the numbers through my Reverse DCF screening logic…

To produce my desired 15% CAGR over the next 5 years, Spotify would need to grow revenues:

→ 32.1% per year in a bear scenario with 17% free cash flow margin, 2% dilution, and 18x exit multiples (unrealistic)

→ 23.7% per year in a base scenario with 17% free cash flow margin, 2% dilution, and 25x exit multiples (still unrealistic)

→ 17.8% per year in a bull scenario with 17% free cash flow margin, 2% dilution, and 32x exit multiples.

The last scenario is not impossible, but quite difficult considering how Spotify has grown +14.5% over the last 3 years and is poised to grow +9.6% in the next 12 months.

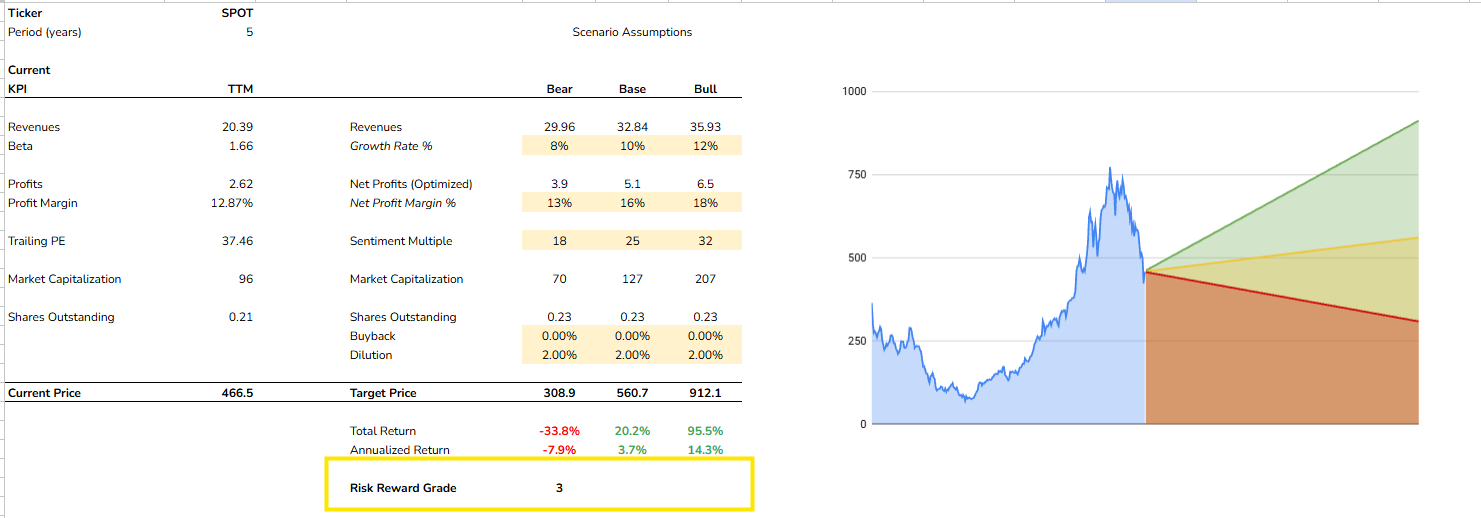

A Risk-Reward of 3/10

Is what emerges by inputing the following 5-year assumptions into our RR model:

Bear Scenario Assumptions:

8% 5-year Revenue CAGR (driven ARPU dilution from Global South, pricing fatigue, ad slowness)

13% Earnings Power (GM stalls at ~34%, OL limited)

18x Exit Multiple (re-rating as growth decelerates to single digits)

+2% Net Dilution Rate per year

Bull Scenario Assumptions:

12% 5-year Revenue CAGR (ADS inflection + pricing + continued sub growth)

18% Earnings Power (GM expands to ~37%, OL kicks in)

32x Exit Mutliple (market rewards profitability and platform expansion)

+2% Net Dilution Rate per year

Under these assumptions, the RR would turn favorable around $373 per share, meaning -20% from here.

What would bring me back

If I had the opportunity for a 1:1 with the new CEO, here’s what I’d ask to spot potential new catalysts.

🚀 C1: SAX Advertising hits inflection point

“When do you realistically expect programmatic ad revenue to hit double-digit growth? And at what point does the ad business contribute enough to push Gross Margin above 37-38%?”

🚀 C2: ARPU increase driven by new verticals and use cases

“Daniel’s vision included merch, DTC superfan experiences, ticketing, physical books. You’ve described 2026 as the ‘Year of Raising Ambition.’ So tell me concretely: which new verticals will drive ARPU growth beyond price hikes?

🚀 C3: the old $100B dream

“Daniel’s once mentioned how Spotify will become an Audio giant of $100B in Sales. How do you see this vision now, and how could the company implement a radical business model transformation towards it, on top of the mere incremental innovation on existing use cases?”

Sure, A pullback to the $350-380 range would create a much more asymmetric entry.

But that would not be enough without new growth vectors.

All in all, for now Spotify was one of my best investments.

It truly was a Compounder for me which allowed me to compound my money as part-time investor in the company.

So thank you, Spoty.

Maybe I’ll be back soon, or maybe not. Anyways it’s been a lovely music to play.

If you liked this:

→ Part-Time Compounder Premium doesn’t just get you deep dives like this, but a full Idea Generation Master Archive with ‘Deep-Dives’ alerts showing up anytime, carefully selected among high-quality lists of compounder-candidates

→ I have a few availabilites left to Join AlphaZen™, my full educational program where you get the entire rules-based value investing system I’m using, while directly learning with me to go from unstructured to expert within 12 weeks

➡️ Click here to apply to AlphaZen™

Thanks for your valuable time.

📈

Happy Investing,

Francesco

Loved it. Your journey is full of lessons and I really like the way you think.

I've never been a Spotify fan but you had a thesis and the gut to hold tight and it turned out to be true. Well done!